5.5 Strategy ⭐

This section includes a mandatory Assignment ⭐

Coming up with ideas for improving your product is easy. In fact, as a PM, you will likely be inundated with ideas and feature requests—from your team, your customers, and your bosses. But how will you decide which features to develop, and—no less important—which features not to develop? This is where product strategy comes into play.

In the last checkpoint, you learned how a SWOT analysis can help you define a strategic path forward for your product (attack, defend, reinforce, and avoid). In this checkpoint, you'll dive into a few other methods to holistically and effectively address product strategy.

By the end of this checkpoint, you should be able to do the following:

- Explain business strategy methods, including the four Ps of marketing and Porter's five forces

- Use the lean canvas method to determine product strategy

What is a strategy?

A strategy is an overarching vision for what your product should do. Having a strategy in place allows you to focus on your other product work and helps you say no when people ask you to do work that goes against your current strategy.

Product strategist Roman Pichler would tell you that a good strategy finds middle ground between a few forces—your target market (the people who are likely to buy and use your product), your value proposition (the way in which your product solves a user problem), and your company's goals (business targets set forth by your executive team).

Each of these will pull you in a different direction, and it's not always clear how to balance them out. The strategy frameworks listed below will help you balance these out—and achieve a great product. They include the four Ps of marketing, the five forces model, and the lean canvas method.

The four Ps of marketing

The four Ps (or 4Ps) are the main factors that go into marketing goods or services—product, price, place, and promotion. Together, these are often referred to as the marketing mix.

You might be wondering—if this is for marketing, why should product managers worry about it? The answer is that all these forces are part of what will determine whether or not your work will be successful. For instance, if your product does what the market is demanding, but you can't get the price low enough to compete against other products, you won't be able to sell it, no matter how good it is. Considering these factors is an important step in creating your product and continuously strategizing for its success.

Product

Your product is the thing you're selling. It needs to solve the problems that people are facing. It's more than the product today—it's also the product's future, your customers' futures, and how that relates to similar products in the market. This factor also impacts all of the other factors. For instance, if your product is really expensive to make, you may be forced to sell it for a higher price. If your product is limited by regulation, you may only be able to sell it in certain places.

Price

The price is what consumers pay for your product. Products have both a real value and a perceived value. The real value is the amount consumers pay for it, the amount they make or save from it, the costs that go into using it, and anything else that can be directly translated to dollars. Your product also has a perceived value—does the product really merit the amount paid for it? Are customers satisfied with it?

Place

The place is how and where a company sells its products. You want to make sure your product is available to buy from the places where consumers are. In the physical world, this means setting up distribution chains and placing your product in stores. In the digital world, this means you want to make it easy for your product to be accessed—on your website, in an app store, on search engines, or anywhere else consumers might be.

Promotion

Promotion is about what you actively do to get the attention of your customers. It's partly the messaging that you use to describe and explain your product to others, such as on your website or Instagram feed. It's partly how you promote your product using specific channels, like paying for advertisements in Google search or in Facebook's news feed. This could also include customer education if your product is complicated to use or novel.

How would you use the four Ps to evaluate the strategy of your product? Examine each P in detail, and ask the following questions:

- Who is my target audience? What benefits does my product provide for my audience?

- What's the right price for my product? Are consumers getting the value they paid for?

- How are we selling the product? Is our product everywhere that our customers are?

- How are we promoting our product? How will consumers learn about it?

As simple as it may look, the four Ps are a valuable way of holistically thinking about your product. If you neglect to consider any of these four, your product—and your job—would soon be in trouble.

Porter's five forces

Michael Porter's five forces framework is another popular method of evaluating a company's strategy. This method focuses on the environment in which a company is operating. The forces are the power of your suppliers, the power of your customers, the threat of substitute products, the threat of new entrants, and the competitive rivals already in your market.

Together, these five forces give you a picture of your ability to serve your customers and achieve your company goals. Learn about each of them below.

Power of suppliers

The power of suppliers in tech products is the power that infrastructure and labor hold over your product. If you use Amazon Web Services as your technology provider and they hike their prices, it could be cheaper to just pay them rather than migrate to the competing Google Cloud Services. If your service depends on people like Lyft or Uber drivers, you'll often be in tension with them, trying to keep them happy while also attempting to limit your costs.

Power of customers (buyers)

Your customers have power. For example, in B2B products, you'll be under pressure to "just add this one feature" so your sales team can close a key deal. In most products, your customers have power when they can easily switch from one product to another. Making products that are unique and deliver high value to customers flips this power to your advantage. Other methods, such as loyalty programs, create additional advantages that make it harder for customers to switch away from your product. As a PM, having a keen awareness of the competitive landscape will help you identify where it may be easy for your customers to switch and where you may have advantages that you can build on to strengthen your position.

Power of substitute products

Some products are threatened by substitutes. For example, you can easily change cell phone carriers by porting your phone number from one carrier to another. Changing your email address is more difficult because you can't easily port an "@gmail.com" address to "@yahoo.com." You could recreate your address book in Yahoo mail, forward all your saved mail from Gmail, and create a transition process to push your regular correspondents, mailing lists, and other email users to your new Yahoo address, but it is time-consuming and cumbersome. Games are another example of a product that has lots of substitutes—people generally enjoy playing lots of types of games and will fluidly move between them.

As a PM, you should be concerned about the power of substitute products, or in other words, the cost and level of difficulty of switching from your product to the competition. You should also consider how customers judge the value or uniqueness of your product against their other options.

Power of new entrants (competitors)

If your product space is successful, it's sure to attract new entrants into your market. Hopefully, there are some barriers to entry, or your product is unique enough so it is difficult for other companies to compete with you. For example, a patented technology, customer lock-in, or exclusive access to specific markets or customers could help protect you from competition.

Apple's app store is a great lock-in tool that would prevent people from leaving for a competing smartphone ecosystem. Apple's singular control of the iOS ecosystem is considered more secure than the Android model and results in fewer fraudulent or dangerous apps being distributed.

As similar, competing products enter your market, you will also see more price competition. This could erode your profit margins unless you can respond by reducing your production costs. Margin pressure reduces your ability to grow or even stay in business because your attention and resources will shift away from innovation or market expansion to meeting new competitive threats. You should always be looking out for ways to proactively respond to competition, whether defensively (such as reducing production costs) or offensively (such as developing new unique features that increase your value proposition to customers).

Power of competitive rivals

You should always be aware of your competition. In particular, you should look out for changes in your competitors' value proposition, advertising and promotion, and changes in the ratio of use of each of their products. Cell phones are a great example. Apple once had a huge advantage in terms of design, but it has since faded. Today, most cell phones look and feel very similar, so the competition is focused on other variables—price, size, battery usage, and so on. If you were a PM at Apple back in the day, what would you do to maintain your design advantage or create new advantages? How would you have stayed ahead of the competition? Conversely, as a PM for another phone company, what would your goals be?

Overall, the key consideration in the five forces model is to understand what's pushing and pulling your company along. These forces are affecting your company from the outside, so you need to look outside to understand them, and respond effectively.

Lean Canvas

The Lean Canvas is a business template developed in response to older frameworks like the five forces and four Ps. It is based on another tool, called the Business Model Canvas. A Lean Canvas uses a single-page, nine-block format to help you get your ideas out quickly so that they can be shared with others.

Since the older tools were made before the internet and mobile technology affected business strategies, this is a popular tool with digital products. It was developed to be succinct, fast to create, and easy to update. It's especially useful for startups creating their first product or companies who are creating new products. This is what it looks like:

Each of the nine blocks in this template serves a specific purpose. Below, read about the various sections, presented in the order in which they should be filled out.

Problem

In this block, list your customers' top problems. One of your primary goals as a product manager is to solve user problems, so keep a specific group in mind. Keep a more detailed list of customer problems and opportunities elsewhere, but list just a few high-value ones here ("top three" is a good rule of thumb). Take a minute to think about existing alternatives that attempt to solve the same problems.

Customer segments

Your top customer segments are directly tied to your problem. Consider these first two sections together. If you have a problem that is not related to a customer segment (target audience) or vice versa, you should get rid of it. Specifically, think about the early adopters of your product—they'll be a subset of one of your customer segments. Analyzing who they are and why they are quick to adopt your product may offer unique insights.

Unique value proposition

Next, jump to the middle column and consider why customers come to you to solve their problems. Why is your solution better than your competitors'? Do you help your customers save money or time? Do you give them access to opportunities?

Your value proposition should be:

- Relevant to the customer

- Different from your competitors

- Easy to explain to a customer (why are you different?)

Start with one or two high-level concepts, such as "saves customer time doing X." This will help you get started on developing your product with a clear goal in mind. You'll continue to refine your value proposition as you work to validate and define the business opportunity.

Solution

When it comes to a solution, you'll have to guess until you get it right. This is the starting point for your first hypothesis. Test early and often, and don't be afraid to prove that a solution doesn't work. It's less costly and less frustrating to do this at this stage—which is why phrases like "fail fast" are popular mottos in the lean startup space.

Also, consider multiple solutions. You might come up with a couple of different things, and they all might work, but they also might have different implementation costs, be more valuable, or be easier to explain to customers. The best solution strikes a balance between multiple considerations.

Channels

Where are your customers? What's the best way to reach them? This is your starting point for marketing outreach. Focus on just a few channels initially. You'll probably want to start with the easiest and/or cheapest ones so you can test your messaging, value proposition, and target audience. As you learn which channels are the most effective, you can better focus your sales and marketing resources on what works well.

Revenue streams

Most products are not initially profitable, but you should know enough about how you expect to make money. What will it take to become cash-flow positive? What kind of profit can you hope to achieve? How, and how much, will your customers pay? Keep in mind that you may need to use different revenue models (such as discounts or free-for-a-while) to attract your first customers. Then, later, you can find ways to transition to a sustainable business model.

Cost structure

What will it cost to build this product? If your product is an internet-based service, what will be the monthly cost with a minimum number of customers? How is that cost expected to grow with additional customers?

Startups often talk about their burn rate—the amount of money they spend each month before they start generating revenue—as a way of thinking about the total amount of resources required to get their product into users' hands. You may need to do some modeling with collaborators from finance or accounting to see when you'll break even or begin to turn a profit. Considering this helps you determine if you have enough capital to get there.

Key metrics

As discussed in a previous checkpoint dedicated to business metrics, you and your stakeholders must decide how to measure success. First, consider what some of the common metrics for your industry or product type may be. Second, ask yourself what key metrics specific to your product you should be tracking. It's tempting to focus on user or customer metrics alone, but those don't always indicate a healthy business. So think holistically about your product, business models, and goal. And set meaningful metrics.

Unfair advantage

Many consider this to be the hardest part of Lean Canvas, and it should be filled out last. This block refers to your secret weapon or unique business advantage. An unfair advantage is a good thing when you are the one who has it. For instance, if your competitors find your product difficult to replicate, that's your unfair advantage.

What do you have that will give your product an edge? Is it new technology? The experts working with you? Tight relationships with key customers? Whatever that advantage is, it has to be something that can't be bought or duplicated.

Using the Lean Canvas

The video below by Alanis will provide a deeper understaind of the Lean Canvas Model

Think of each block of the Lean Canvas as "something to be validated." You can test your model part by part, finding out where it works and where it doesn't. Don't hesitate to revise sections. If your customer interviews prove that your solution is lacking, come up with some new ideas and try again. Everything is interconnected, and finding the right balance between the various categories is important.

Before you scroll any further, grab a pen and paper and try to fill out a Lean Canvas page for Uber when they were just getting started. Then, scroll ahead to see what a hypothetical Lean Canvas for Uber might look like. Testing yourself against an example will give you a sense of whether or not you've mastered how to use this important tool.

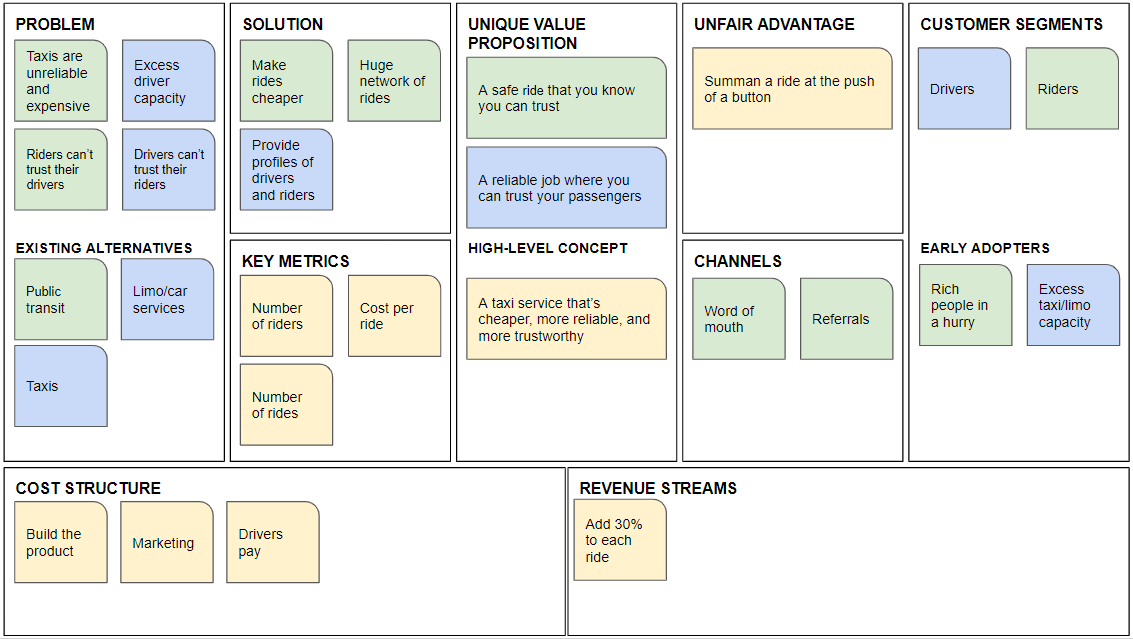

Lean Canvas—Uber example

Here's a hypothetical Lean Canvas for Uber's initial launch. A good practice is to use colors when referring to specific groups. In this case, green is used for riders, blue for drivers, and yellow for both/neither. If this was your company, which block would you want to test first?

Reflecting on these models

If you've been reading closely, you might have noticed these different strategic models all have unique characteristics, as well as some shared commonalities. Here are a few to note.

Tools matter

You can put a group of smart people in a room and try to come up with a business strategy, but it's unlikely to produce the best results. Tools like the Lean Canvas or the four Ps of marketing are true-and-tested tools to guide your strategic thinking process. You can treat these as individual assignments or use them to structure a discussion among your stakeholders.

Competition matters

Your product exists in a world with current competitors and future entrants. You need to pay attention to the landscape of competing and substitute products. Even small differences like a slightly lower price or design change can sway customers' sentiment.

Find your advantage

Products can be copied, and features can be imitated. Find an advantage that distinguishes you from the competition. What are you doing that can't be copied? What advantage do you have today? Will that advantage disappear in the future if a stronger competitor or new technology enters the market? Long-lasting business success comes to those who find, communicate, and maintain a unique advantage.

Assignment 05 ⭐

Present a business strategy analysis using two of the methods reviewed in this checkpoint. Read the following instructions carefully to ensure you are meeting all the assignment requirements.

- The Presentation must be in a slide deck, a medium article or a notion page.

- The analysis should cover one of the following products:

- Zomato (or a similar food delivery app)

- Candy Crush Saga for mobile (or a similar mobile game)

- Salesforce (or a similar B2B software product)

- One of your analyses must be a Lean Canvas. For the second, you may choose between the four Ps of marketing or Porter's five forces.

- Document your work in a slide deck or other document you can easily present while screen sharing. You may make a copy of this Lean Canvas Slides Template or use any other method you find useful in order to walk a viewer through your analysis.

Be sure to use these methods to discuss your product's value proposition, the competitive landscape, and the strategy going forward. End with an answer to this question: What will you focus on next as the product manager for this product?

Upload your article/slides and submit a link to it on the respective Slack channel.

Submission

Submit your links in the slack channel #assignment-05